Once you submit the loan application—including your preferred loan and lender—our team reviews the request and responds with a quote that you can take back to your client for their review.

Often, the quote will be based on your preferred loan and lender. Occasionally, we may recommend a different option that's a better fit for your client's needs and circumstances.

We understand how crucial it is for you to feel comfortable interpreting lender quotes and explaining them clearly to clients. This guide walks you through how to read the quote and present it back to your client.

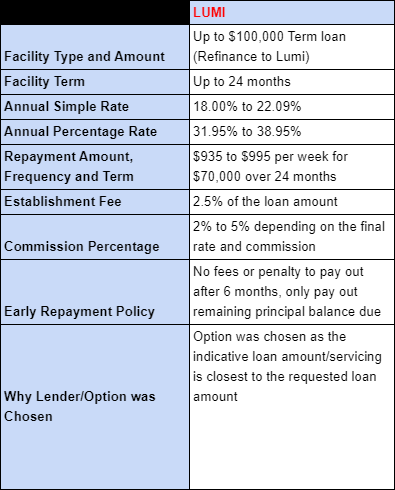

The quote box

Our admin team will email you a breakdown of the offered loan, displayed in a table, similar to Lumi's example below.

What’s inside the quote box

Facility type and amount

The name of the loan product, and the maximum capacity the lender can offer. This may differ from the client’s requested loan amount, as lenders will only approve up to their repayment serviceability limit.

Facility term

The requested or maximum loan term the lender will offer, in months.

Annual simple rate and annual percentage rate

Presented as a range (i.e. 18% to 22.09%) because a final and precise rate won't be available until the lender issues a formal offer. Remember, you should always quote conservatively and quote both interest rate types, to help put the APR rate into perspective for a client.

Some lenders will an exact quote and interest rate during a ‘lender workshop,' but these are conditional and subject to credit checks.

Repayment amount, frequency, and term

The repayment frequency is the weekly or monthly dollar amount to be repaid, and the repayment term is the timeline for the loan repayment, in weeks or months.

This repayment amount is the loan principal, i.e. the loan amount requested by the borrower and offered by the lender. This is often less than the maximum loan capacity allowed within the selected loan product.

For example, you can see in the above quote that while the client may be eligible for a facility type and amount up to $100,000, but as the client had only requested $70,000 the repayment figure is based on the latter amount of $70k.

Establishment fee

Fees charged by the lender to cover the establishment and admin costs to write the loan. Less commonly known as an application or drawdown fee.

With some lenders, and Lumi in particular, many of their loan products and rate tiers allow you to adjust the establishment fee upwards from the standard 2.5% to 4% . As a referrer this can then allow you to increase your commission up to 1.5% if in turn you chose the maximum establishment fee.

Commission percentage

This is total commission paid out by the lender to Valiant as a percentage. Presented as a range as the final amount is dependent on the lenders formal offer. Noting that this does not account for the payable commission that you will earn. To calculate your commission use this formula.

Early payout terms

The conditions and allowances for paying out a loan early. Usually a key selling point, and important to show that the client has flexibility within the loan facility.

Why lender/option was chosen

Our reasoning for selecting this loan and lender above all others. Essential to relay these reasoning back to the client when discussing the quote to give the client confidence that this is in their best interests.

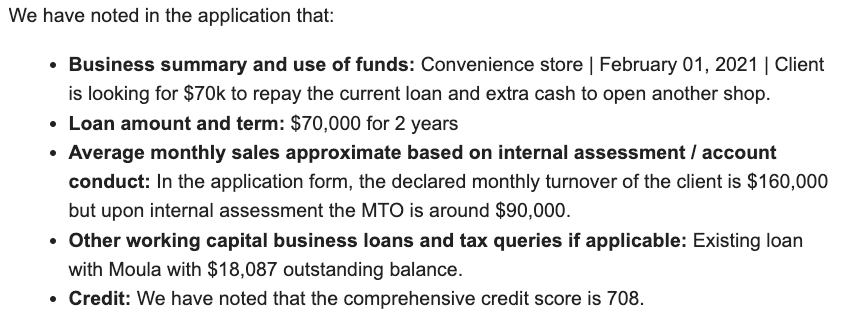

Client and loan summary

After the quote, we also pass along the summary of our discovery on the client’s background and circumstances as documented both by the referrer and through Valiant’s internal assessment.

This is important because:

- It will highlight basic information about the business operations and funding need, as well as a view of their credit score and existing exposure.

- It will highlight any discrepancies between the internal assessment and the information provided in the application form which may affect the quote (e.g. turnover or liabilities)